RBA Tracker

Time to shift gears

Please note that this service will now focus solely on the ONLY CHARTS publication, which will at some point shift to a paid publication. The price will be very affordable, particularly given the publication’s high frequency and quality content (in our view!).

All in-depth research is now being published on Antipodean Macro Professional which is aimed at the investor and funds community. Please check it out with a short-term subscription.***

New year, new RBA outlook?

Yes, kind of.

We expect the RBA Board and Governor Bullock to provide a more even handed outlook for interest rates.

Our view is that the shift in Bank of Canada communications is a good blueprint of what to expect (see below). That is, don’t completely rule out the risk of another hike, but suggest that the discussion is shifting to how long the cash rate will remain at the current level.

Bank of Canada provides a blueprint

Major central banks have changed their tone - to different degrees - on the likely outlook for monetary policy to one where the next interest rate moves are likely down.

The RBA doesn’t operate in a vacuum, and central bankers talk all the time. Often the language they use is the same, or very similar.

Inflation developments in Australia also aren’t looking too different to those globally, suggesting that a the RBA’s narrative shouldn’t be in a different ballpark to that of other central banks.

In our view, the Bank of Canada (BoC) provides a good blueprint for what to expect from the RBA next week:

“…the Bank’s Governing Council’s discussion of monetary policy is shifting from whether our policy rate is restrictive enough to restore price stability, to how long it needs to stay at the current level.

But the BoC remains cautious, and we expect the RBA to do the same:

“That doesn’t mean we have ruled out further policy rate increases. If new developments push inflation higher, we may still need to raise rates. Governing Council is concerned about the persistence of underlying inflation. We want to see inflationary pressures continue to ease and clear downward momentum in underlying inflation.”

The Fed and Bank of England both strongly suggested this week that the next move in policy interest rates in the US and UK will be down, but not anytime soon.

Central banks don’t want to have to reverse course

A cardinal sin in central banking from a credibility perspective is the need to quickly reverse policy changes, particularly rate cuts if they turn out to have been premature.

Debate will rage about whether central banks are inherently biased in setting monetary policy.

At times like the present, however, when overall disinflation has been rapid but uneven (i.e. tradables vs non-tradables and goods vs services), it’s clear that central bankers want additional surety that inflation won’t re-accelerate.

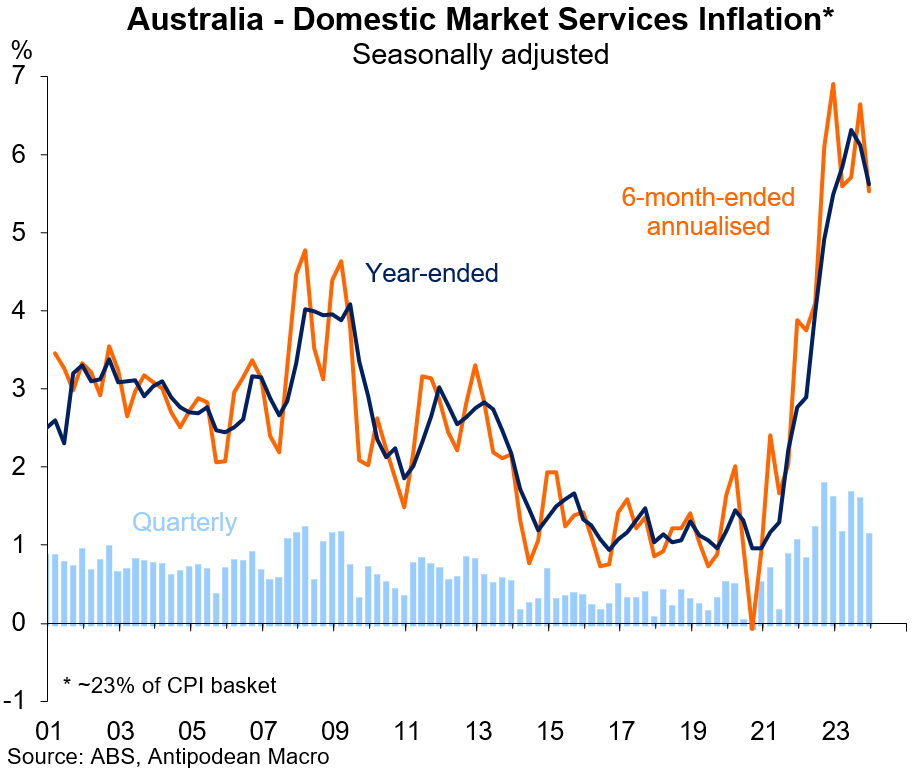

In Australia’s case, the RBA is keenly focused on domestic market services (and rents) inflation which both remained elevated in Q4 2023 (see here for more detail).

In fact, quarterly inflation for most services categories in Q4 remained in the top half of the distribution across all 87 CPI categories.

The upshot is that the RBA is likely to remain cautious on the likely speed of further disinflation.

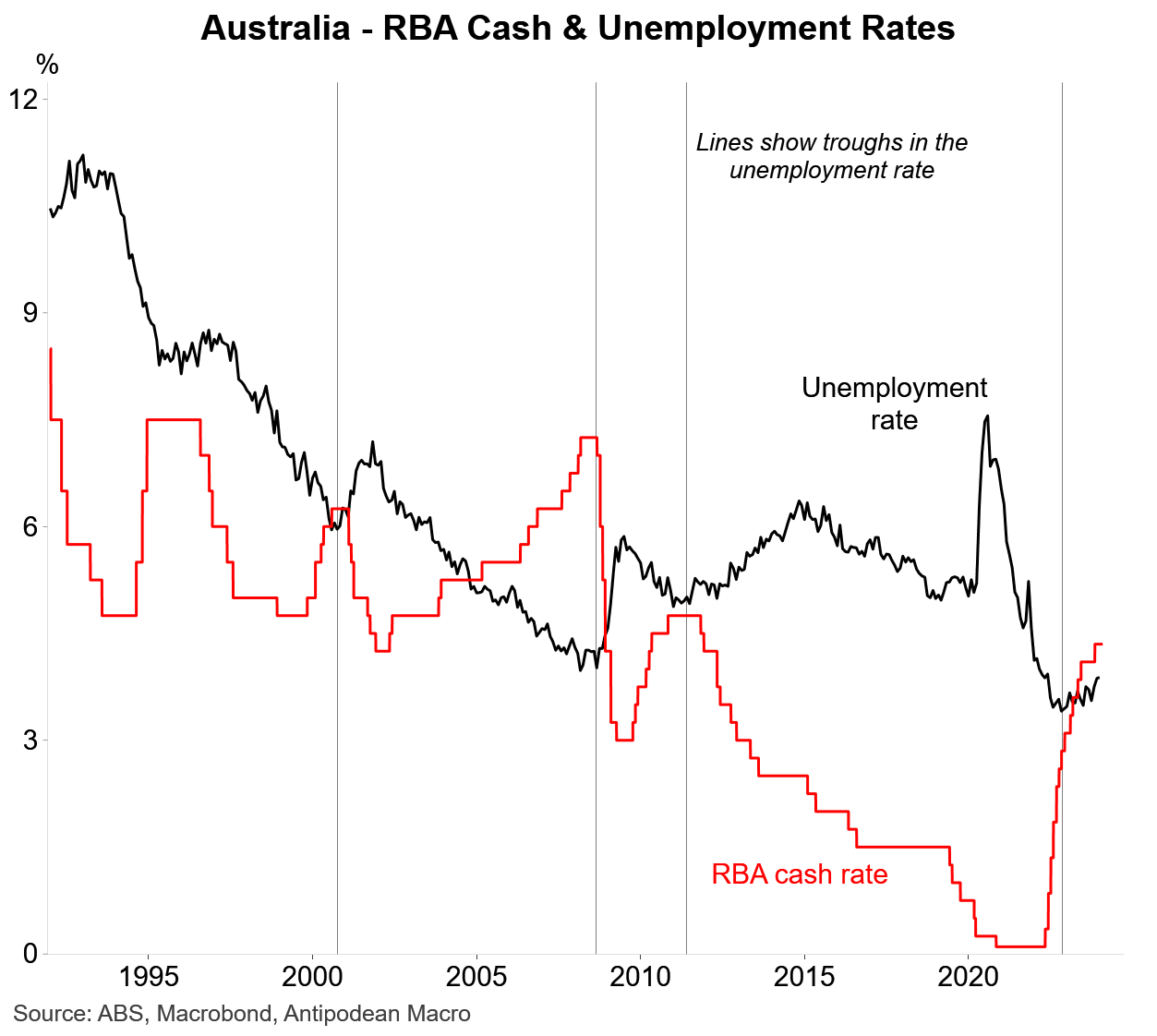

For now, they have the luxury of still-low unemployment to maintain that caution.

Focus will shift more to labour markets

Absent a renewed pick-up in inflation, the focus is likely to turn more clearly to developments in labour markets. Historically, it hasn’t taken long for central banks to start easing monetary policy after the trough in unemployment rates.

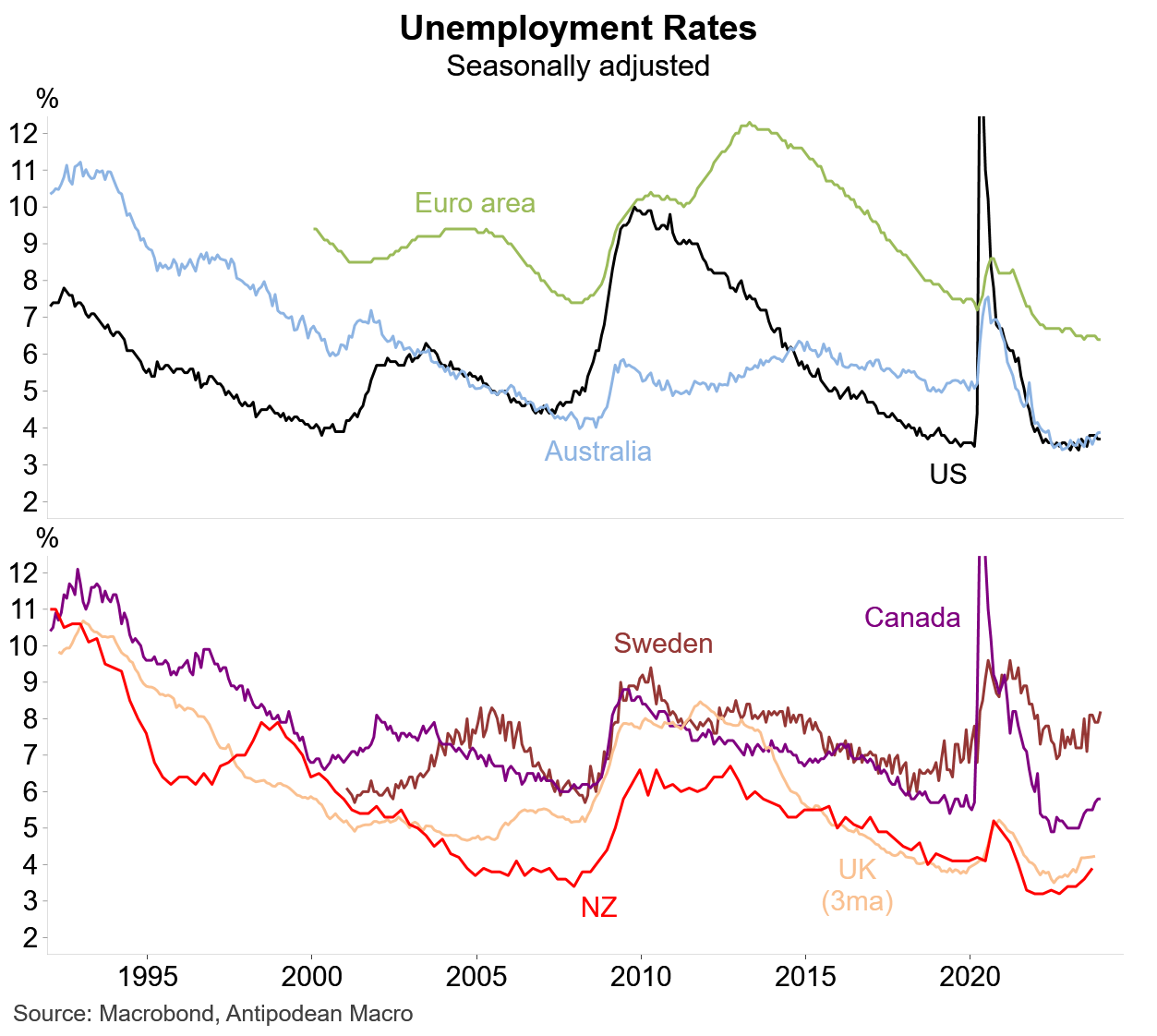

A difference this time is that unemployment rates remain very low and have only been rising gradually in most economies, including Australia.

So, central banks have time on their side, for now.

Market implications - is it already priced in?

The lower-than-expected Australian CPI print this week already resulted in a decline in Aussie bond yields (3yr: -13bps) and a shift in RBA cash rate expectations (see chart).

The result is that some softening in the RBA’s hawkishness is already priced in.

If the RBA does not soften its stance as expected, there is likely to be a knee-jerk back-up in yields.

But there is a risk that the RBA Board gives an inch and markets take a mile.

For the end of 2024, markets are currently pricing in rate cuts of ~150bps by the Fed and ECB, ~110bps of easing by the Bank of Canada and Bank of England, but less than 70bps of RBA rate cuts (and 90bps by the RBNZ).

While that partly reflects the RBA’s lower current policy rate (except compared with the ECB), there is a clear risk that the confirmation of a dovish tone from the RBA results in an outsized reaction at the short end of the curve, at least initially.

This is where changes to the Bank’s inflation forecasts will be important. A shift in trimmed mean inflation forecasts broadly back to those in the August Statement would not be a big change even if the extension of the forecast horizon sees expected inflation gliding down to 2.5% by mid-2026.

As an aside, we think observers need to start paying much more attention to the forecast evolution of quarterly inflation rather than year-ended inflation.

The Bank’s communication last year was all in terms of year-ended inflation not returning to the 2-3% target for a couple of years. That’s fine when current rates of inflation (including quarterly) are sitting well above target.

Our experience, however, is that central banks can quickly change the narrative to focus on shorter-dated measures of inflation to highlight progress on disinflation.