1. The number of homes newly listed for sale in New Zealand continued to increase in March…

2. …leading to a further rise in the stock of homes for sale at the end of the month.

3. Against that backdrop, kiwi housing prices haven’t done much recently.

4. The volume of existing home sales in New Zealand has continued to move broadly in line with housing price growth.

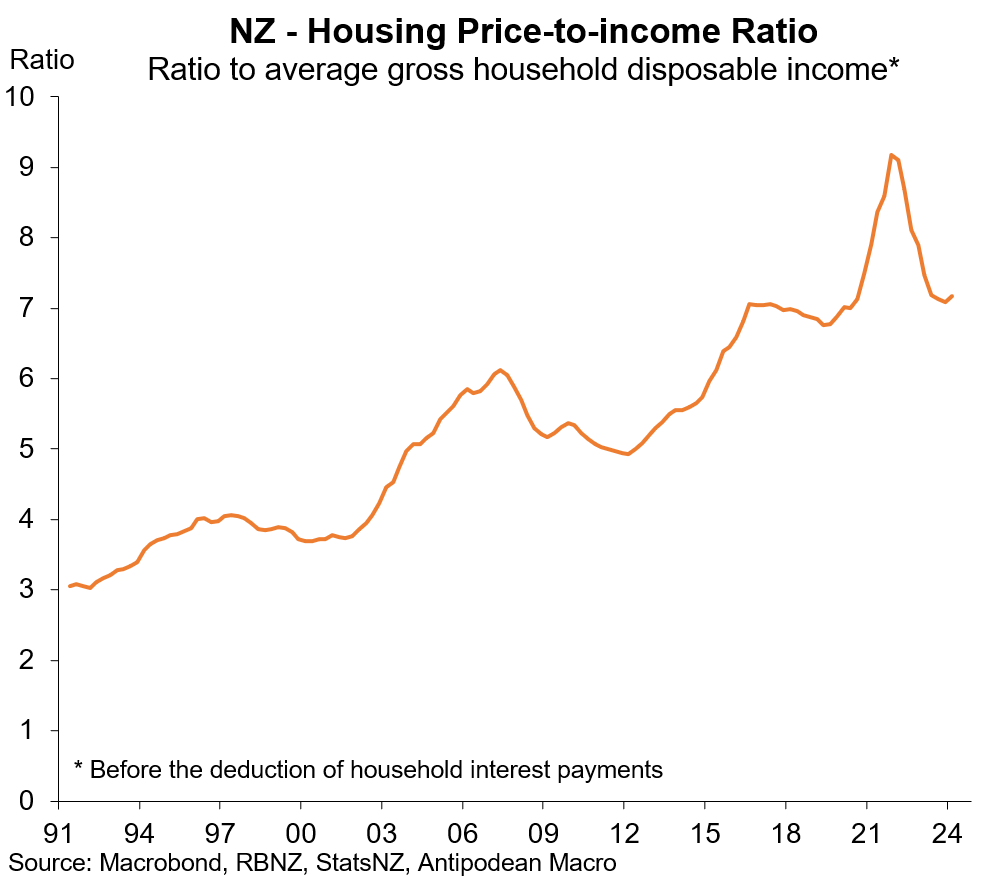

5. Real housing prices and the home price-to-income ratio in New Zealand continue to move broadly sideways.

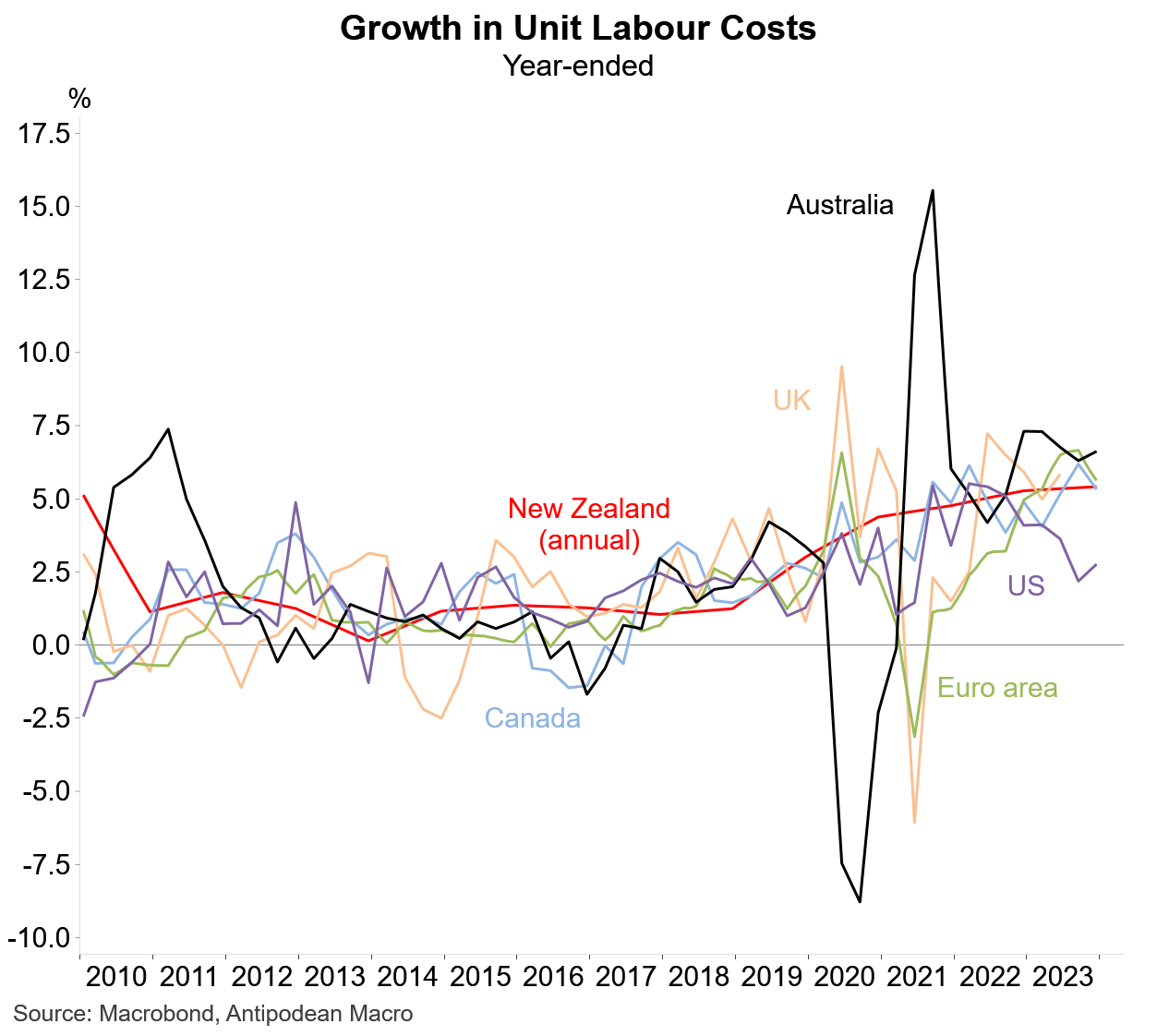

6. Annual data show that unit labour costs in New Zealand rose 5% in the year to Q1 2023.

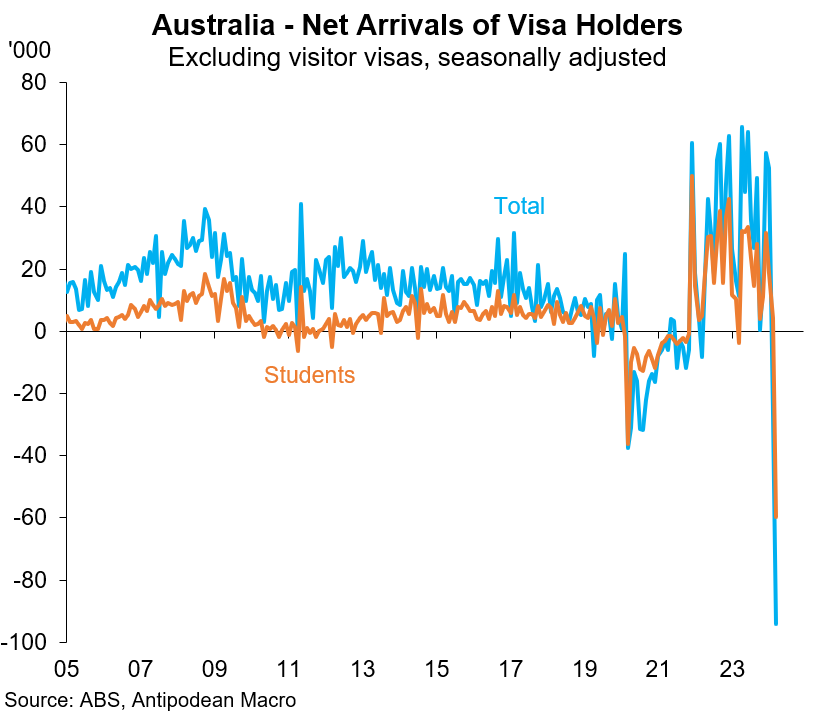

7. The monthly proxy for Australia’s net immigration remained at a high level in the 3 months to February.

8. BUT data to March on net visa holder arrivals could be showing the initial impact of the ‘crackdown’ on student visa grants. While these data are more volatile than data on net permanent & long-term arrivals to Australia, and seasonal adjustment remains tricky, the scale of the drop is eyebrow raising.

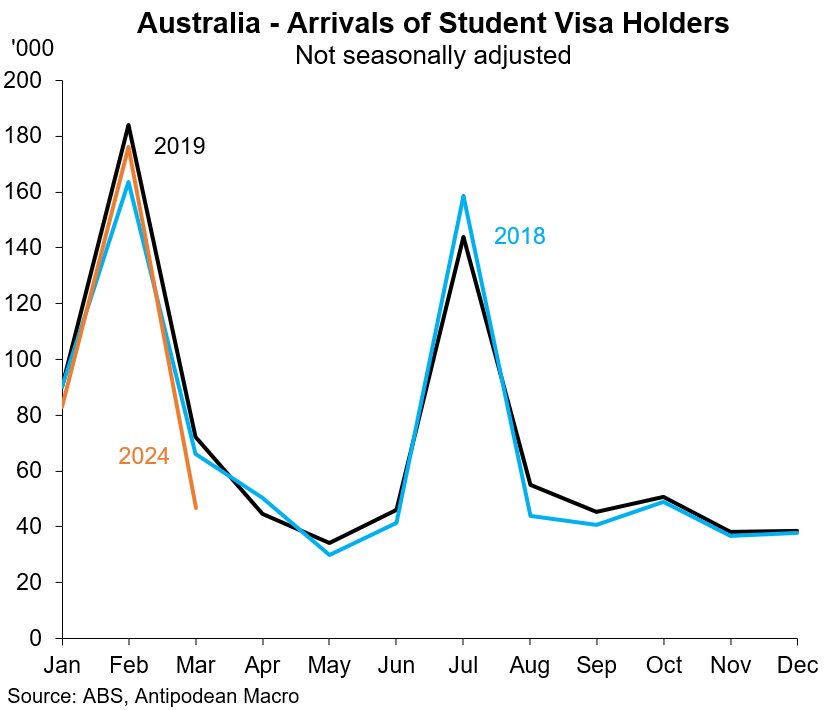

Raw data on arrivals of student visa holders show a much larger fall in March this year than in 2018 or 2019.

9. The share of Australian firms reporting recruitment difficulties continued to trend lower in March.

10. New house sales in Australia picked up a little through Q1 but remained at a low level.

Great content as always Justin. Quick question with the net visa holders ex visitors chart, are you able to explain which visas you included for this? I have tried to replicate the chart myself but was unable to get something similar to what you have shown. Cheers, Anthony.