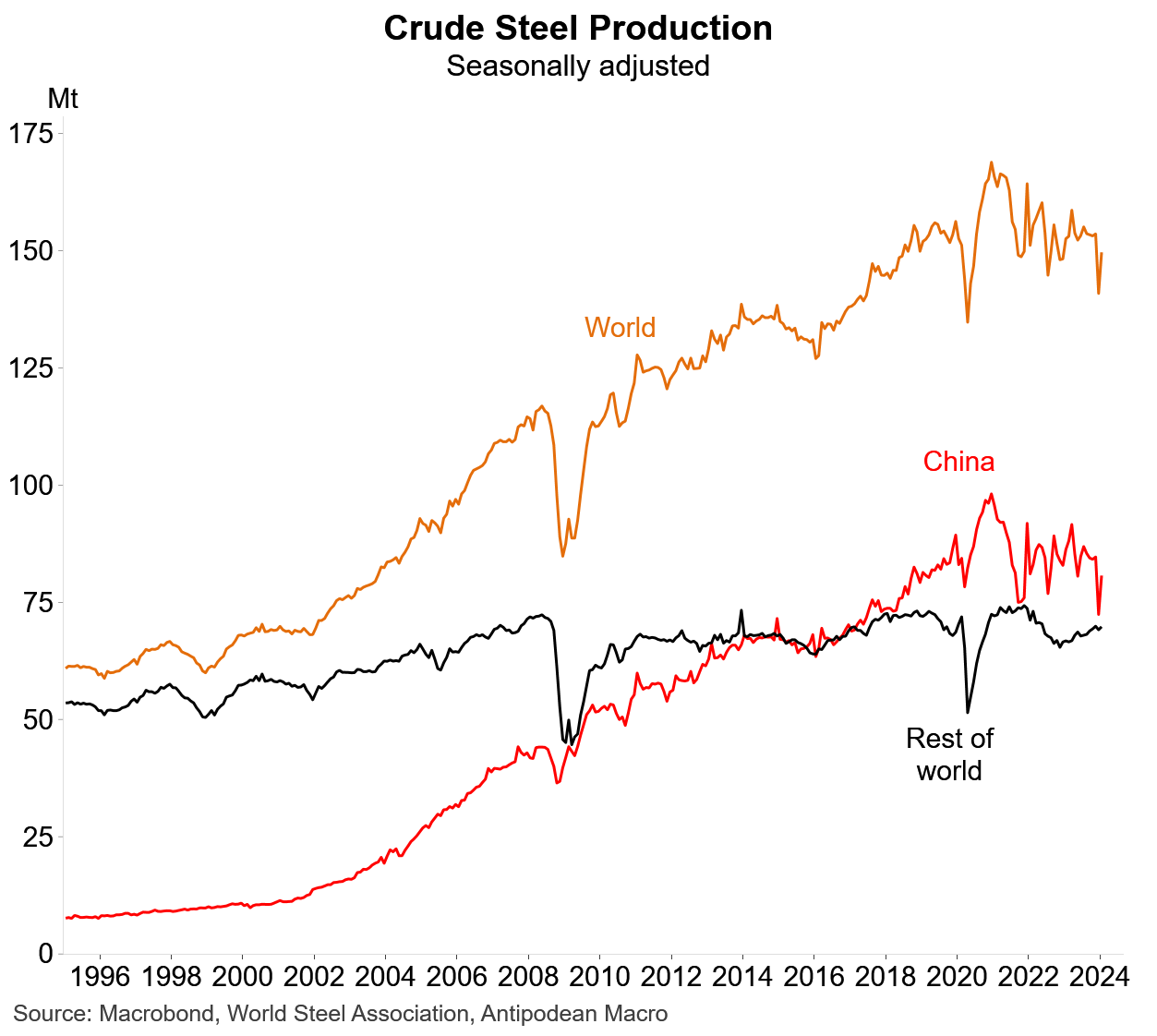

1. World steel production improved in January after December’s plunge - all because of volatility in Chinese production. Stepping back, steel production has trended lower for two years.

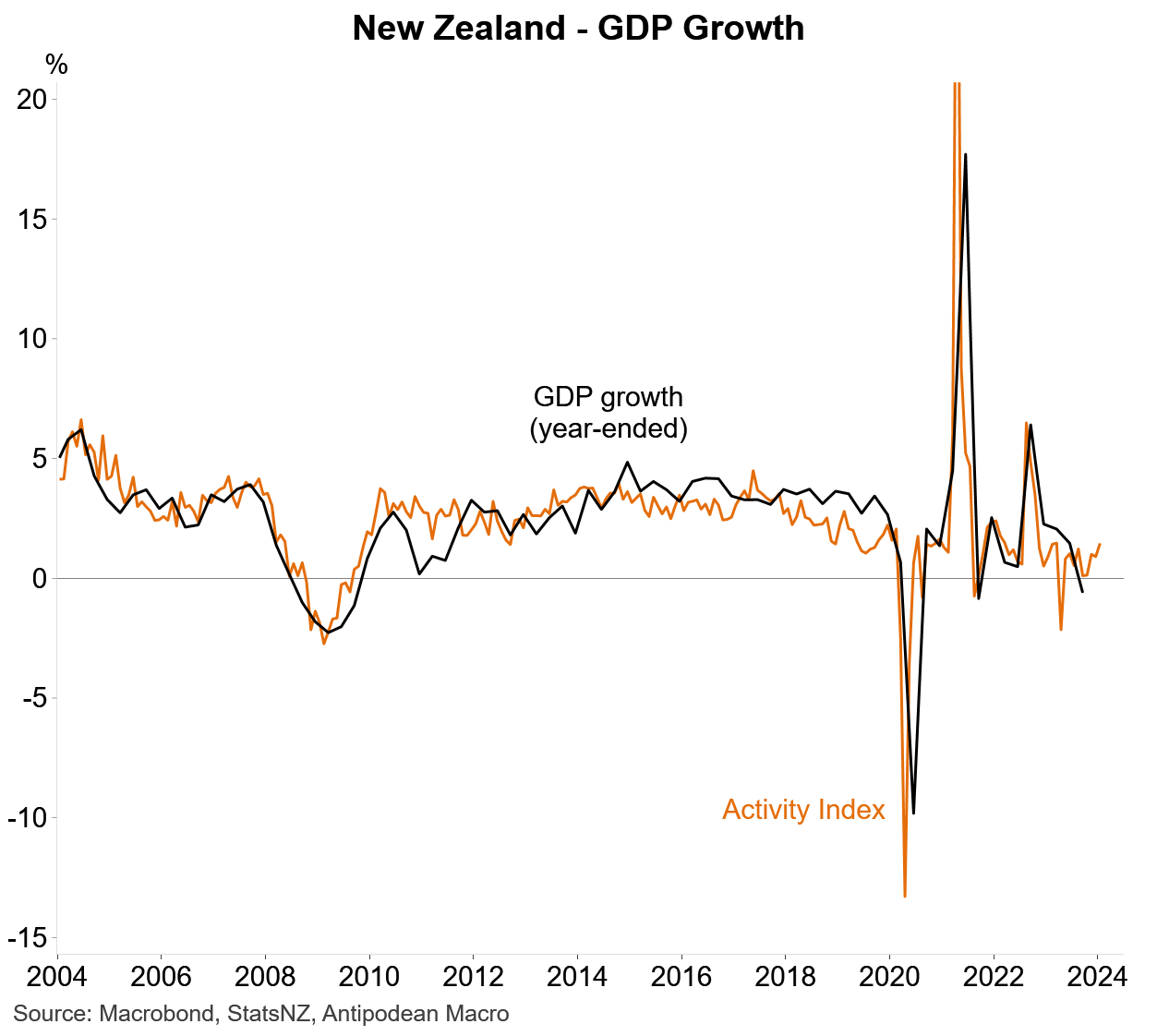

2. New Zealand’s Activity Index rose in January and, along with various business surveys, suggests that growth may have improved a little around the turn of the year.

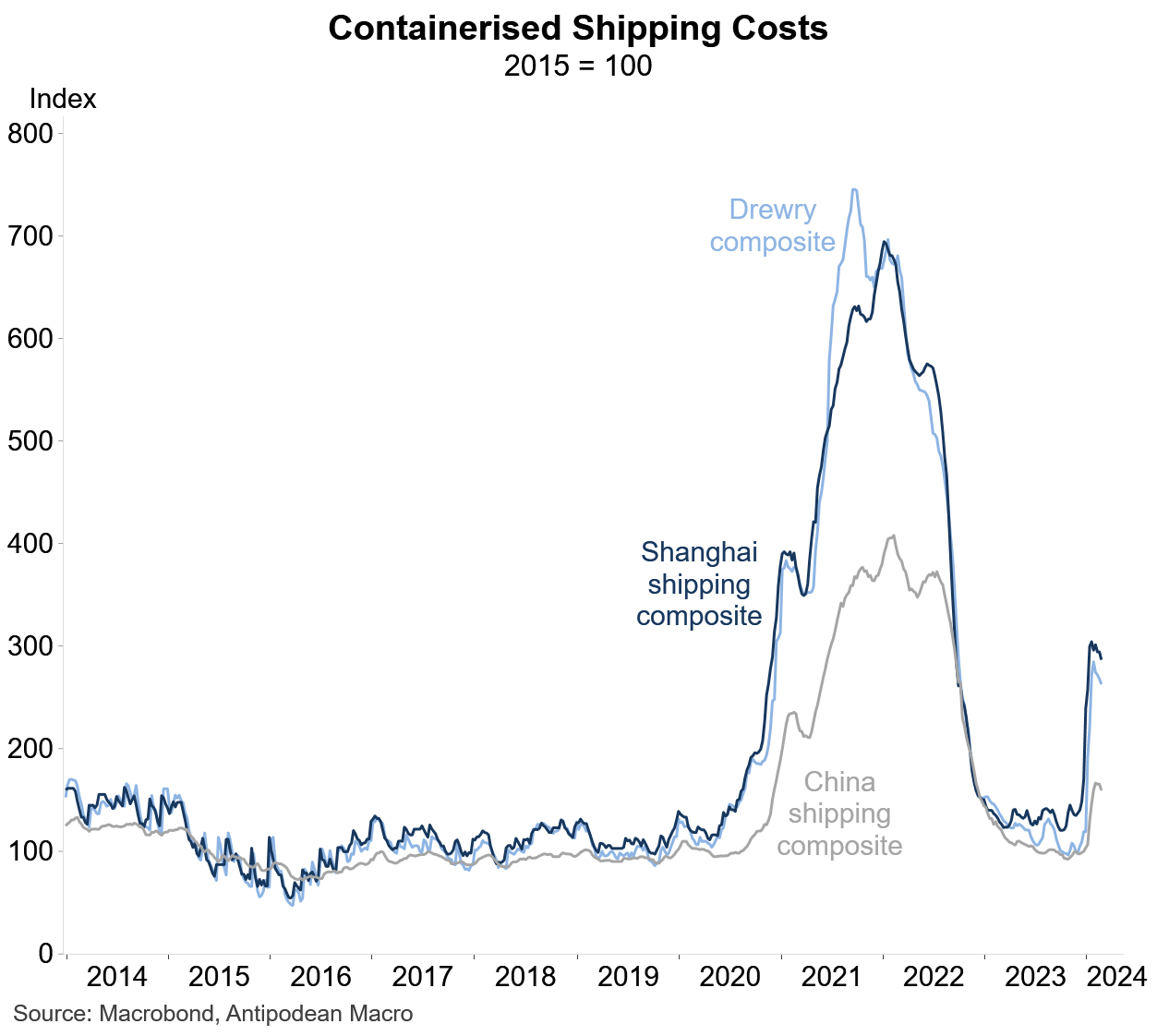

3. Indicators of global containerised shipping costs have fallen a little from recent peaks.

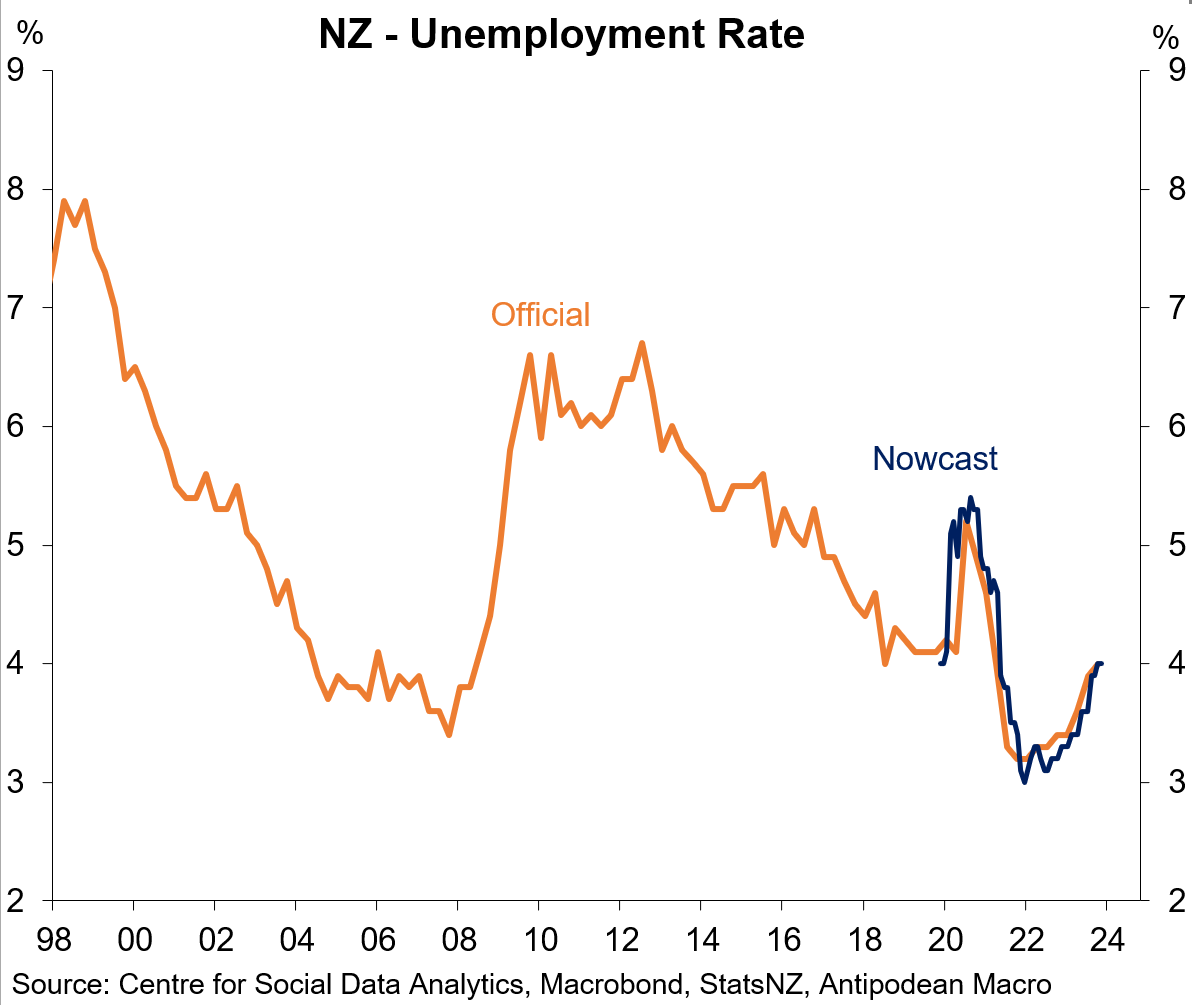

4. The nowcast for New Zealand’s unemployment rate was 4% over December and January.

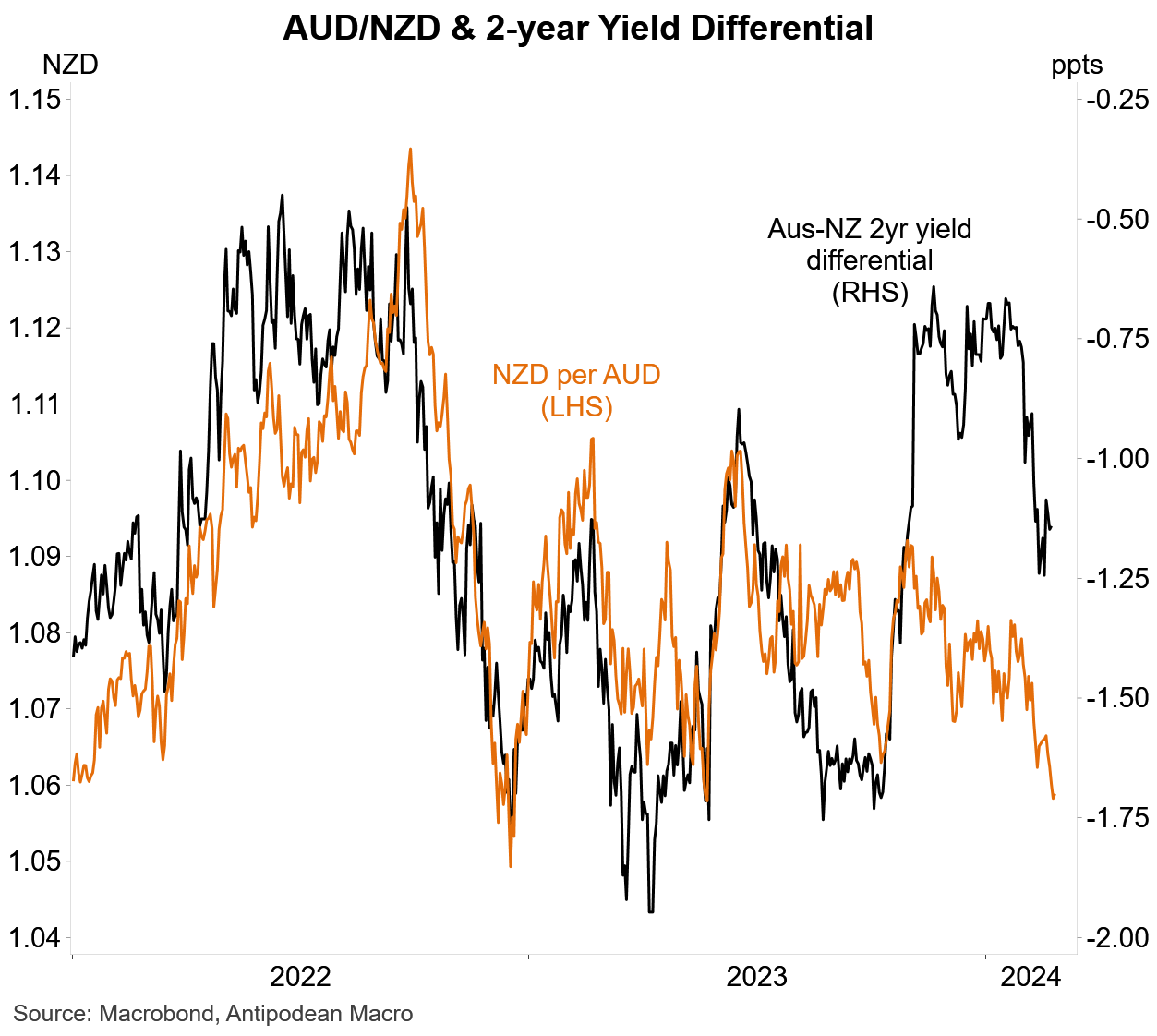

5. The A$ has depreciated against the NZ$ to the lowest level since May last year amid an increase in NZ bond yields relative to Aussie yields

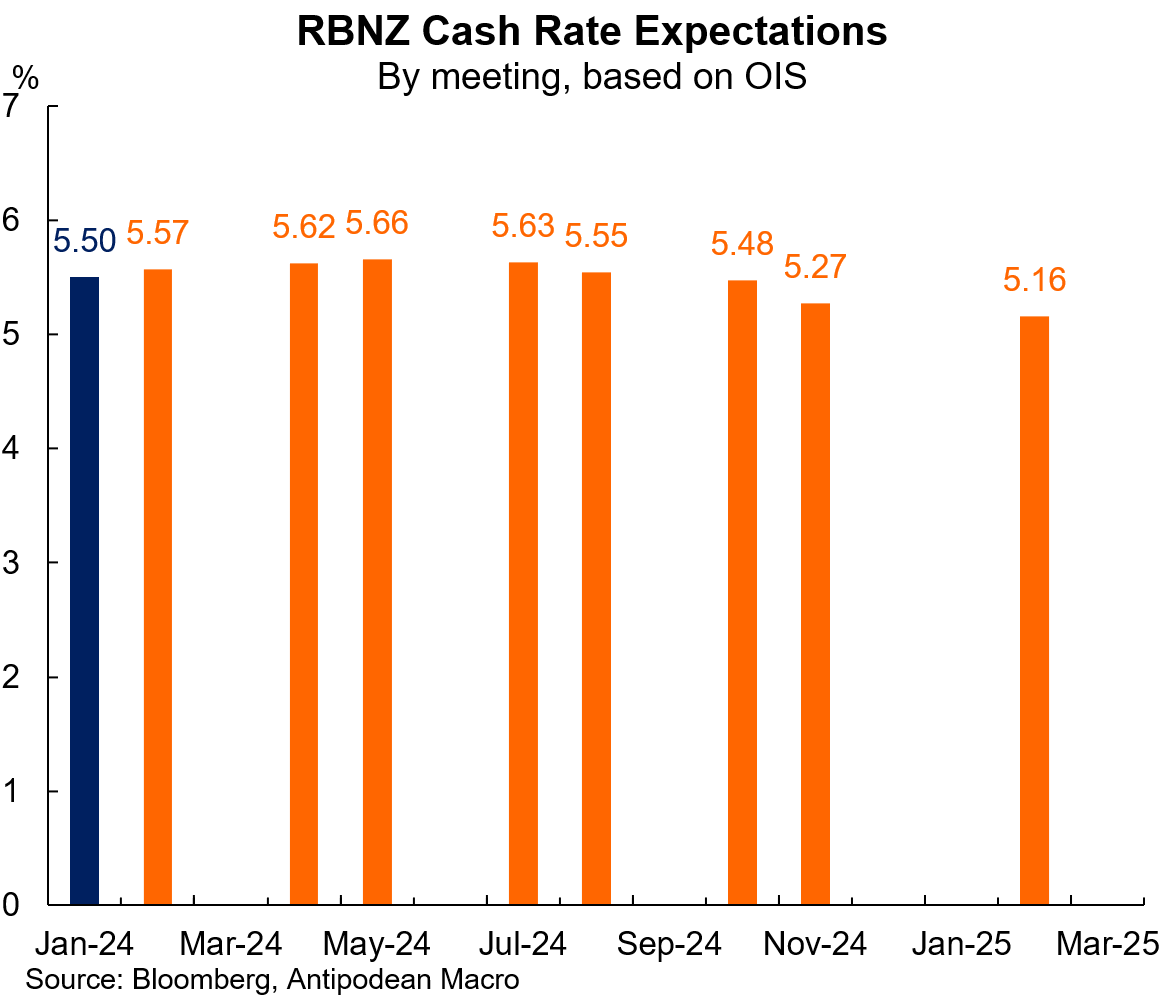

6. Markets are pricing a bit less than a 30% chance of an RBNZ OCR this week. Our view is that the odds of a rate hike are higher than that BUT the MPC should hold off and send a clear signal that interest rates will remain elevated as (domestic) inflation remains uncomfortably high

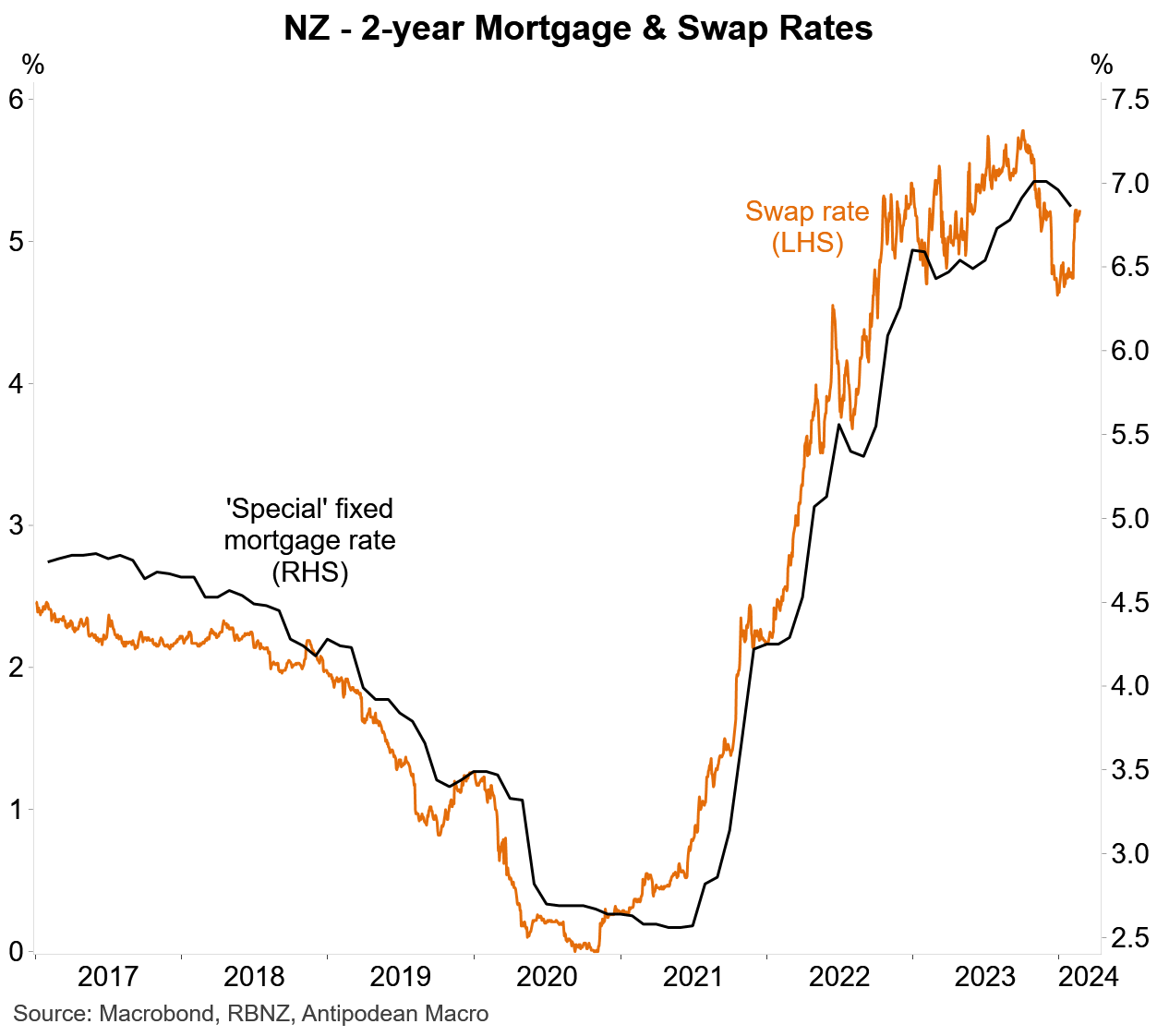

7. Something that has pushed the RBNZ into action before is developments in market interest rates. Swap rates and mortgage interest rates have eased a little which the RBNZ could use as justification to hike and re-tighten financial conditions

8. Back in November the RBNZ’s MPC noted that “[i]f inflationary pressures were to be stronger than anticipated, the OCR would likely need to increase further.“

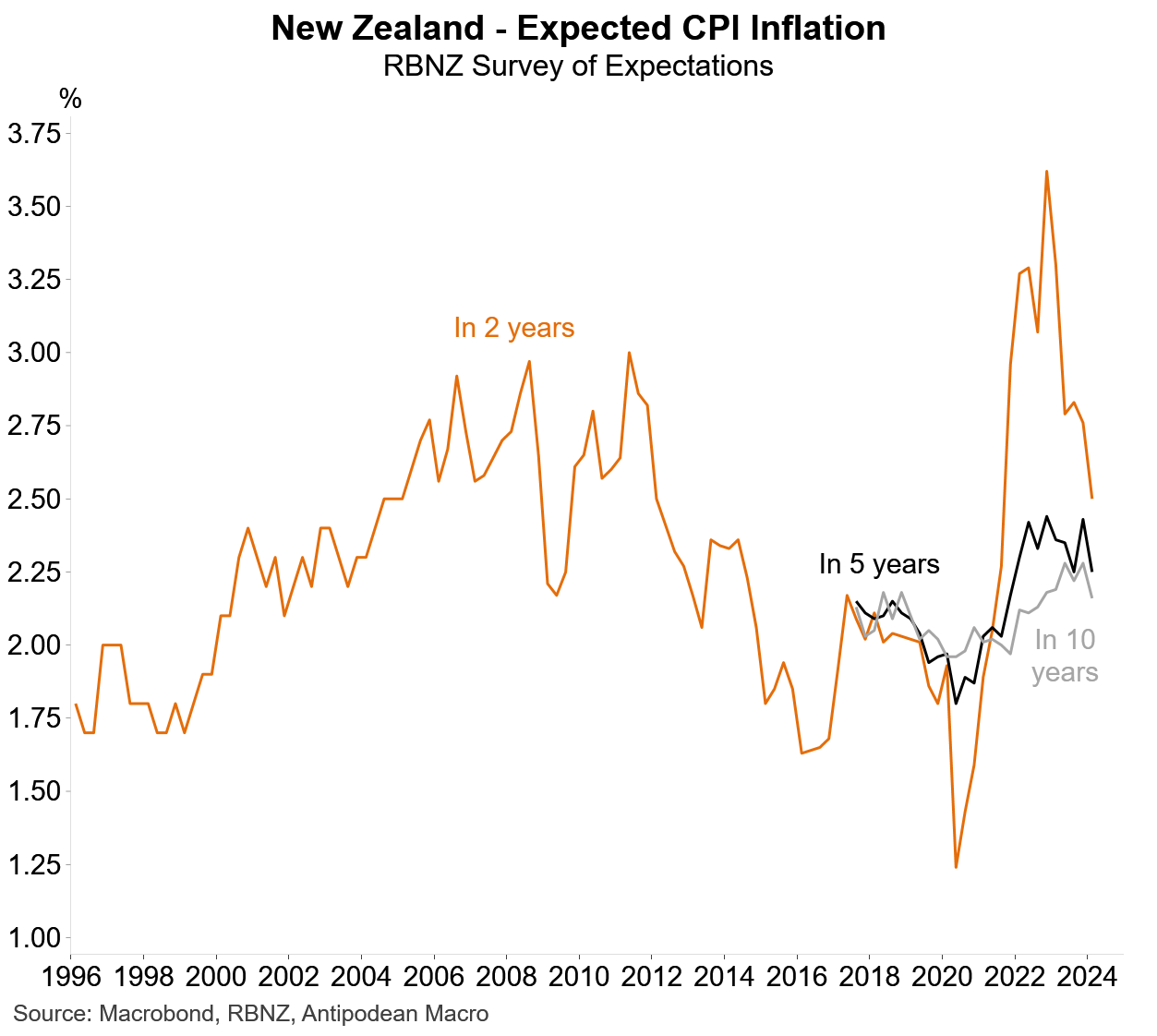

Since then, Q4 headline inflation was lower than the RBNZ expected but non-tradables inflation was above its forecast. Meanwhile, the Bank’s own survey showed some moderation in medium-term inflation expectations (see chart).

So, something for everyone, likely resulting in a close call on the OCR on Wednesday.