1. Aussie firms reported slightly better forward orders in March…

2. …and continued to report that hiring remained above average, though probably not strong enough to keep up with robust population growth.

3. In that vein, Australian businesses continued to report a trend increase in the amount of spare capacity in their operations.

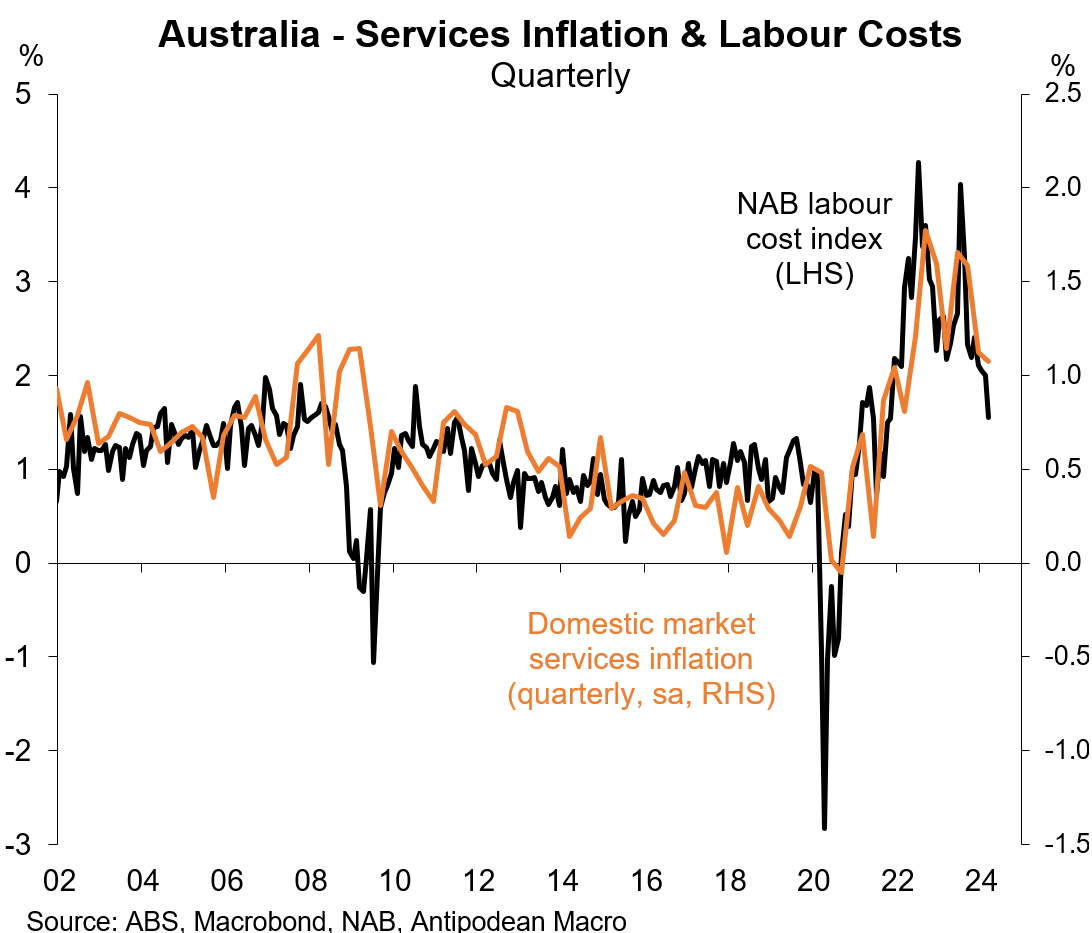

4. Encouragingly, inflation and cost measures in the NAB business survey moderated further in March. Firms’ reported output prices slowed sharply, pointing to the potential for underlying inflation to slow heading into the June quarter.

5. Profitability in Australia has been (partly) supported by an ability of firms to “hide” in inflation. Those days look numbered.

6. As profits growth slows, however, firms naturally look to their cost bases. In that vein, businesses reported another slowing in labour cost growth in March…

7. …which will be news to the RBA’s ears in their plight to dampen services inflation.

8. Aussie households’ views towards buying major household items deteriorated over March and April, unwinding most of the modest prior improvement.

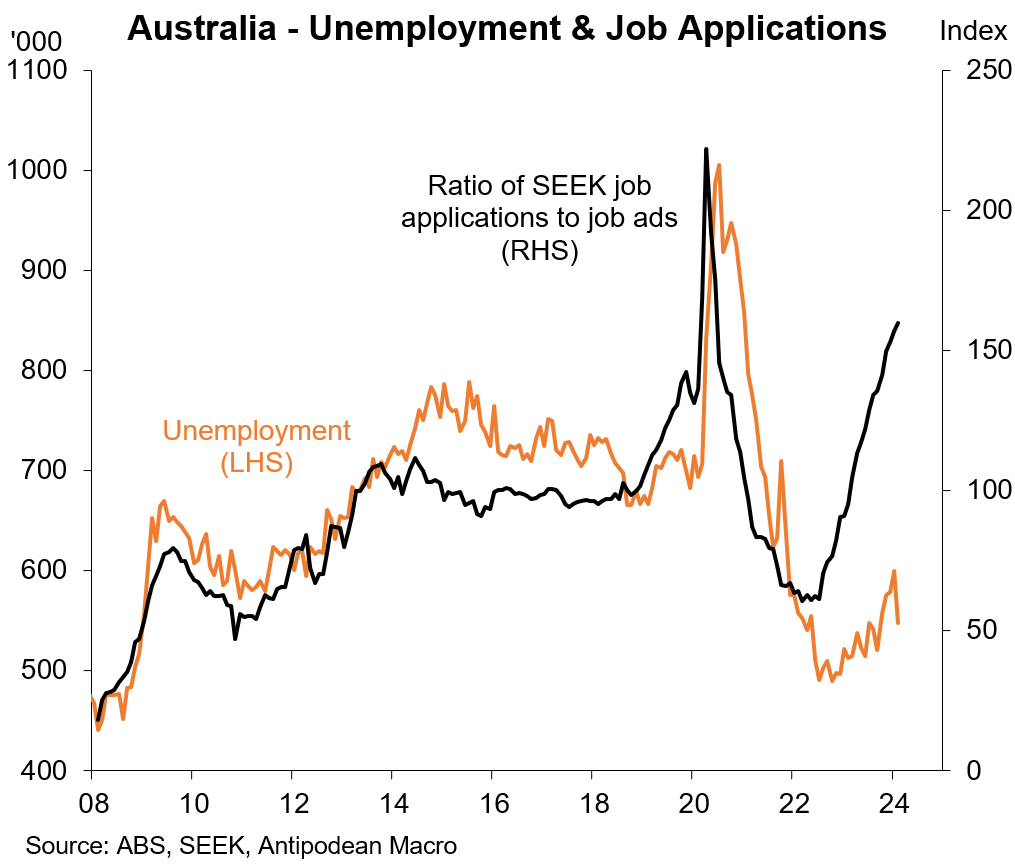

9. The number of new job ads advertised on SEEK in Australia rose 2.4% m/m in March, unwinding the decline over February. Job ads were modestly higher than levels in late 2023. The job vacancy rate (relative to unemployment) rose in recent months, but that is partly because of volatility in the unemployment data.

The ratio of job applicants to job ads (to February) continued to trend higher.

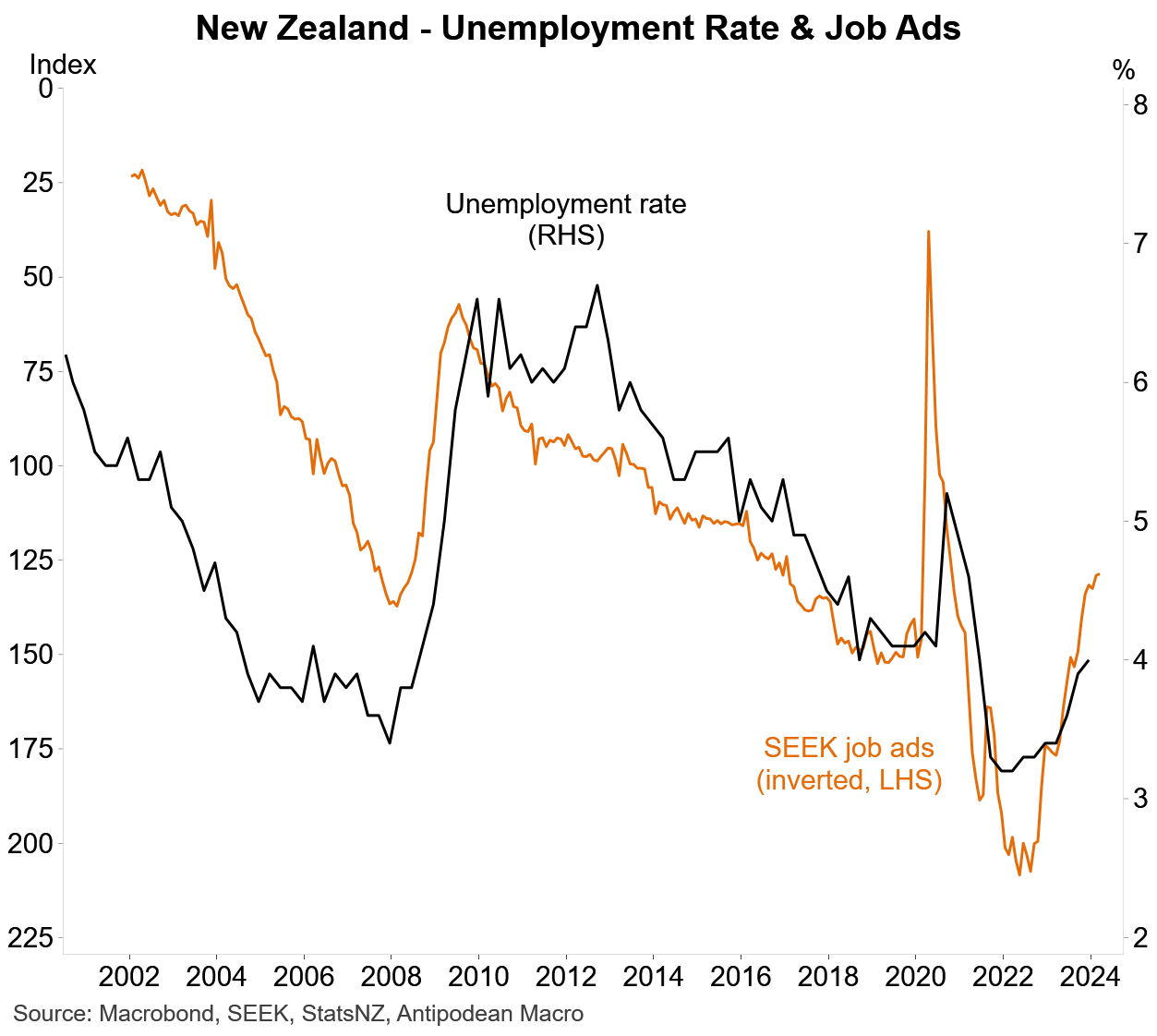

10. SEEK’s new job ads index for New Zealand declined slightly in March - the labour market is still softening.