ONLY CHARTS

www.antipodeanmacro.com

1. SQM data suggest that growth in residential asking rents remained strong in Australia’s capital cities in the March quarter.

2. Growth in CPI rents in Australia has shot higher amid significant excess demand for housing (this chart was inspired by a similar CBA version).

3. Domestic spending using credit and debit cards in New Zealand has been broadly unchanged for a year in nominal terms.

4. Kiwi’s card spending on durables continues to trend lower.

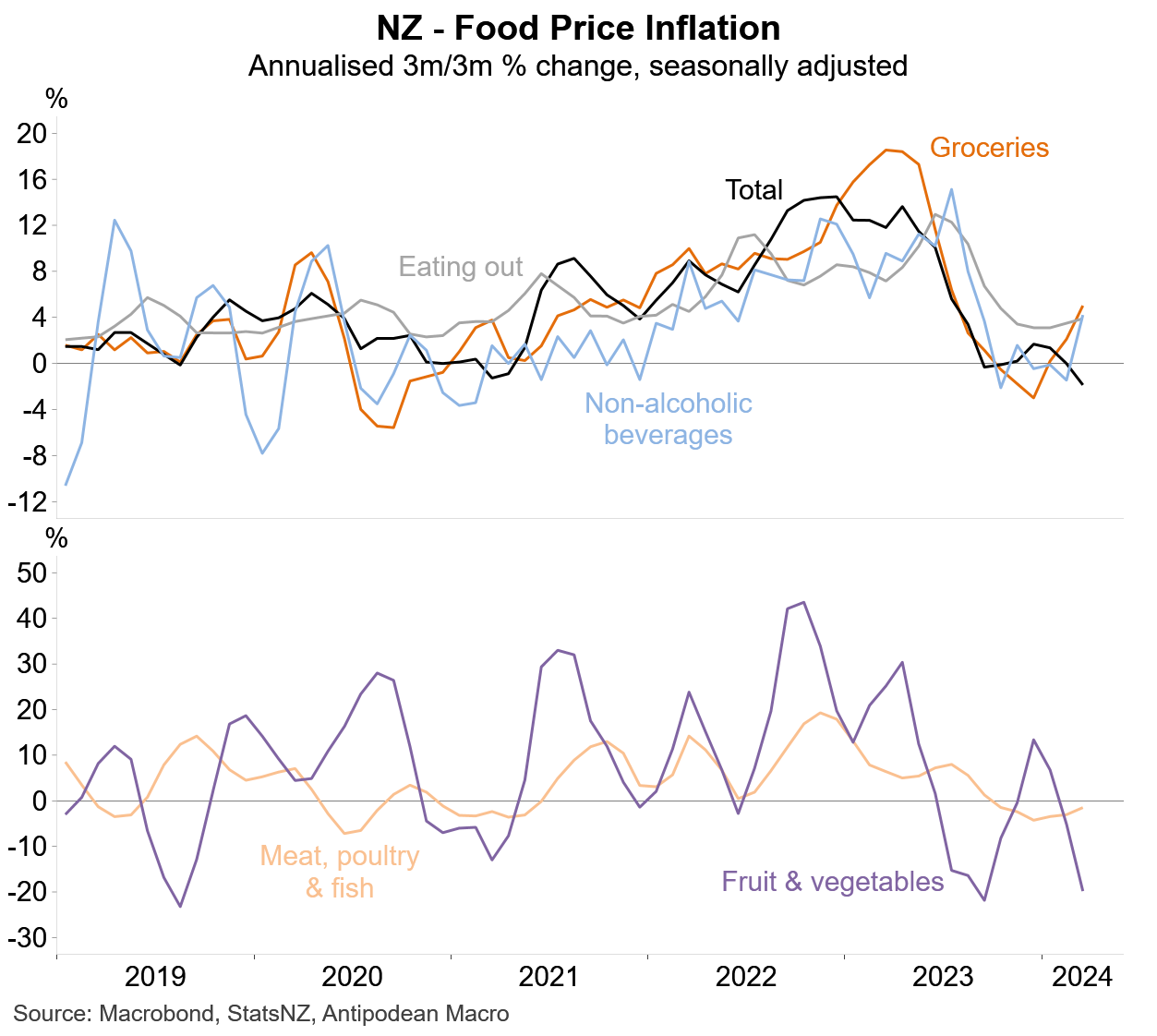

5. Food prices in New Zealand, which have an 18% CPI weight, rose +1.8% q/q in Q1.

After seasonal adjustment, however, food prices declined 1.9% q/q amid falling prices for fresh items. In contrast, prices for grocery items and non-alcoholic beverages strengthened in Q1, while eating out inflation remained close to 4% on an annualised basis.

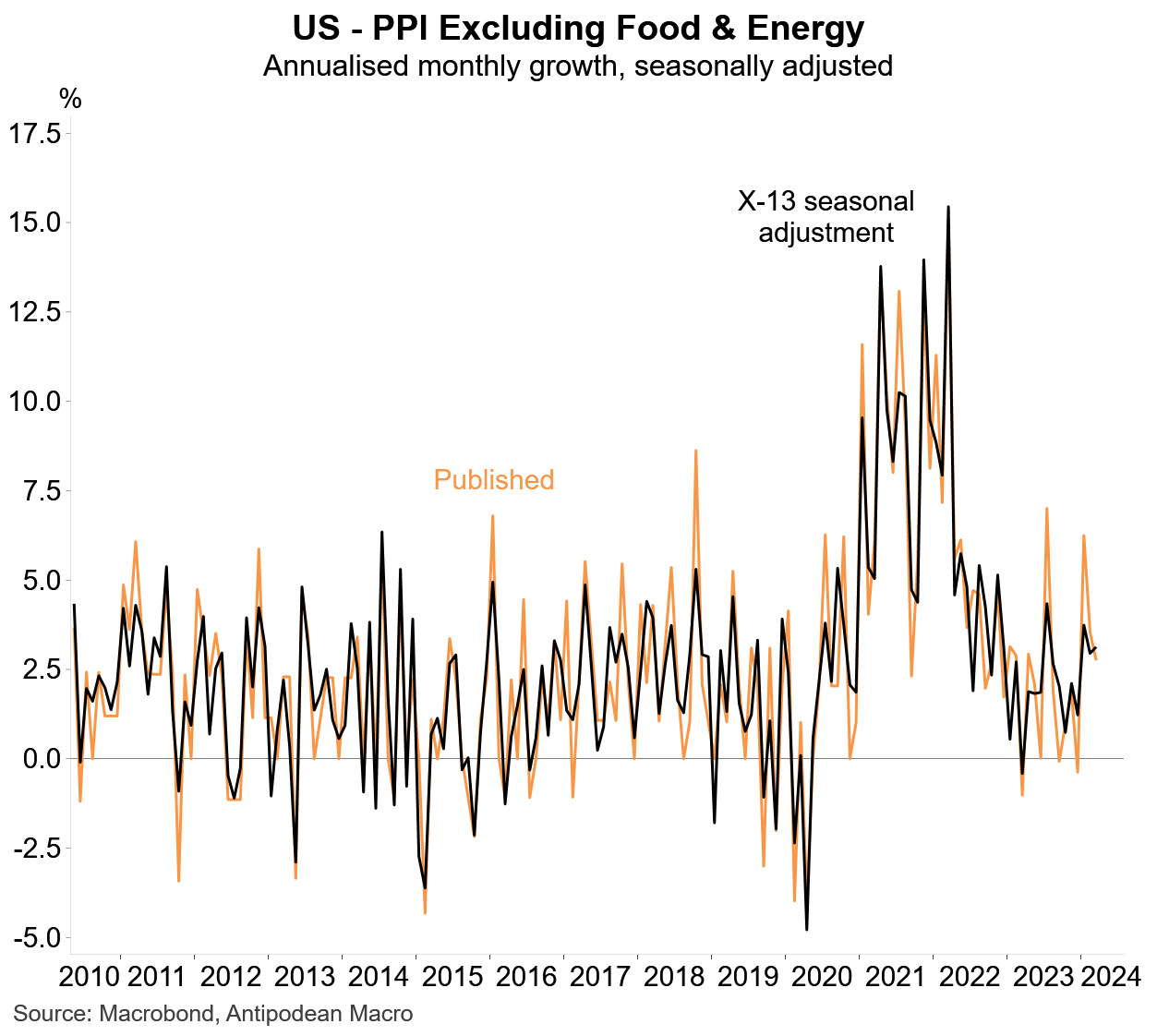

6. Core US producer price inflation slowed in March, but our own seasonally adjusted measure - which has been much less volatile than the published equivalent - remained around where it was in February.

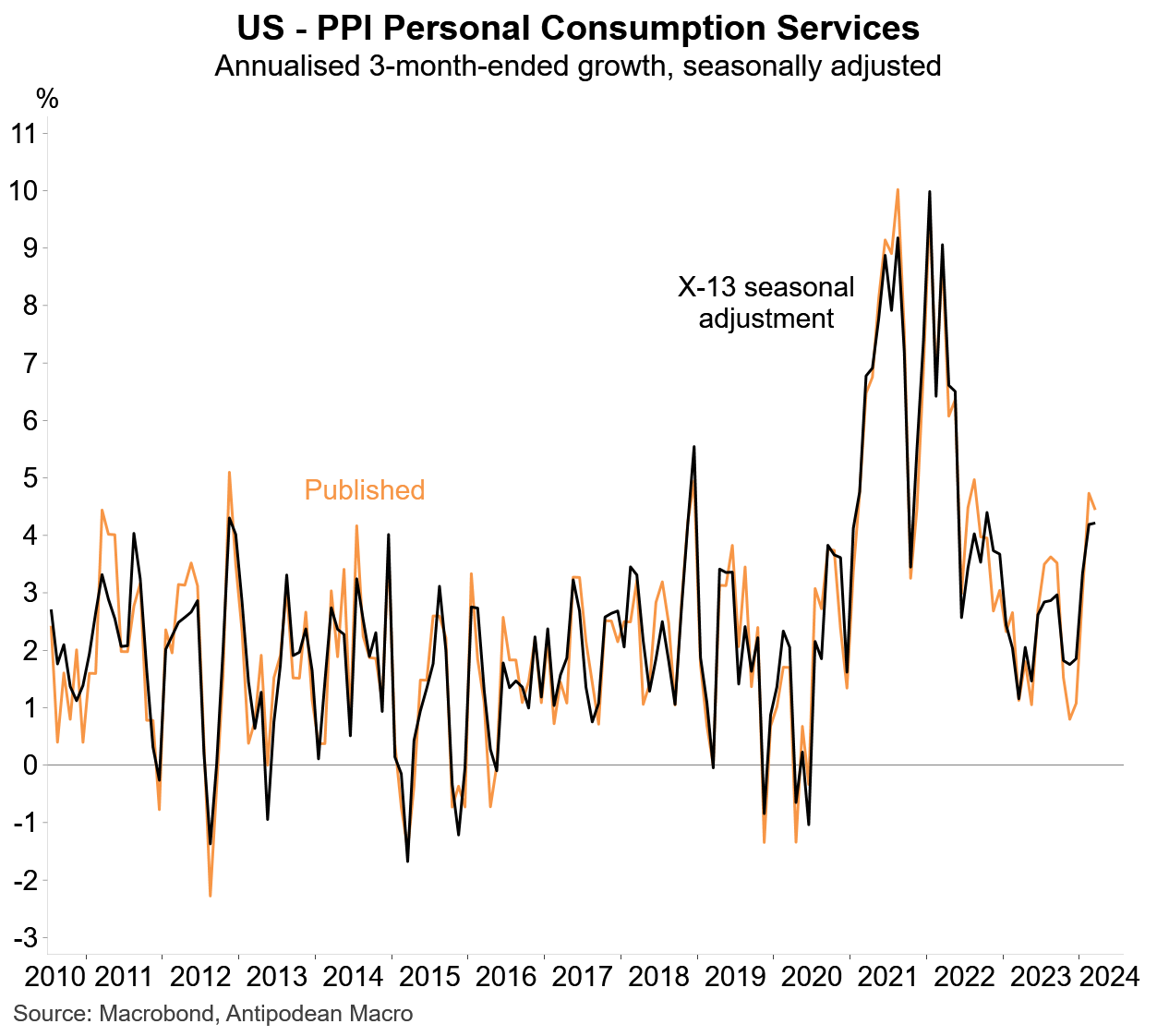

7. That is also true for the PPI personal consumption services measure…

8. …with both seasonally adjusted measures remaining above 4% in annualised 3-month-ended terms.

9. Global containerised shipping costs have continued to decline