ONLY CHARTS

www.antipodeanmacro.com

1. Dwelling starts in Australia rose a touch in Q4 2023 but were at just 153.6k on an annualised basis. This is well short of what is needed.

2. Dwelling completions in Australia are likely to hold up in the near-term given the significant ‘excess’ starts in recent years.

3. For detached houses, the number of completions has picked up in recent quarters.

4. Moreover, there was still a large pipeline of incomplete dwellings in Australia at end-2023, but that pipeline is shrinking.

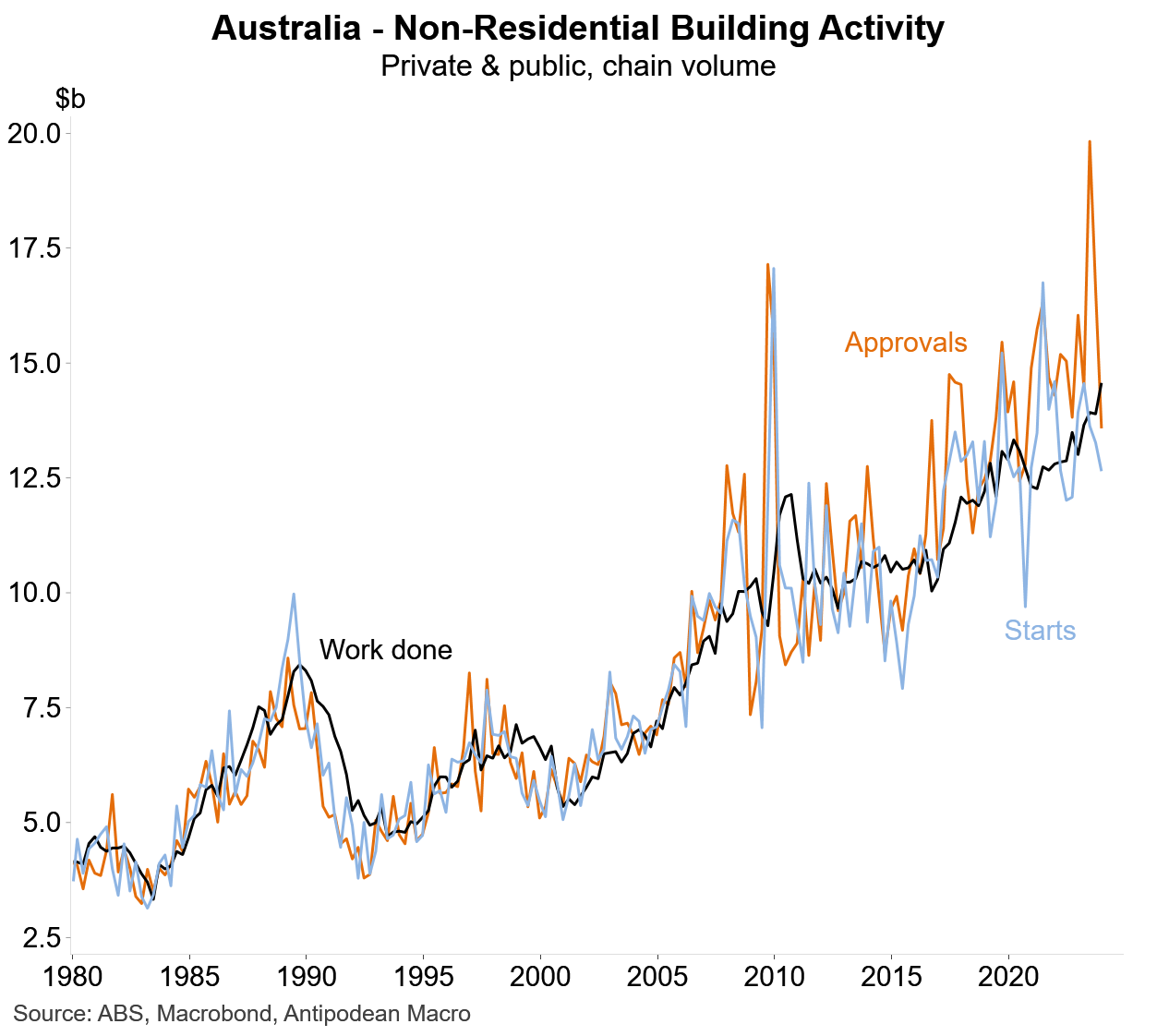

5. Non-residential building starts have noticeably lagged approvals in Australia in recent years (another sign of capacity constraints).

6. As a result, the value of non-residential building work that has not yet commenced has risen sharply (particularly in Queensland and SA).

7. The current run-rate of seasonally adjusted housing price growth in Sydney and Melbourne so far in April remains quite weak (caveat: seasonal adjustment has become less reliable post-COVID).