ONLY CHARTS is only available to paid subscribers.

A 7-day free trial is available below. Group discounts are available here.

Antipodean Macro’s in-depth research is available here.

Today’s Aussie CPI confirmed that underlying inflation remained robust in early 2026. While quarterly trimmed mean inflation of +0.8% q/q was a bit softer than expected, prior revisions meant it was in line with the RBA’s forecast in year-ended terms.

Despite prevailing uncertainty regarding the Middle East stand-off, we expect the RBA Board to increase the cash rate next week.

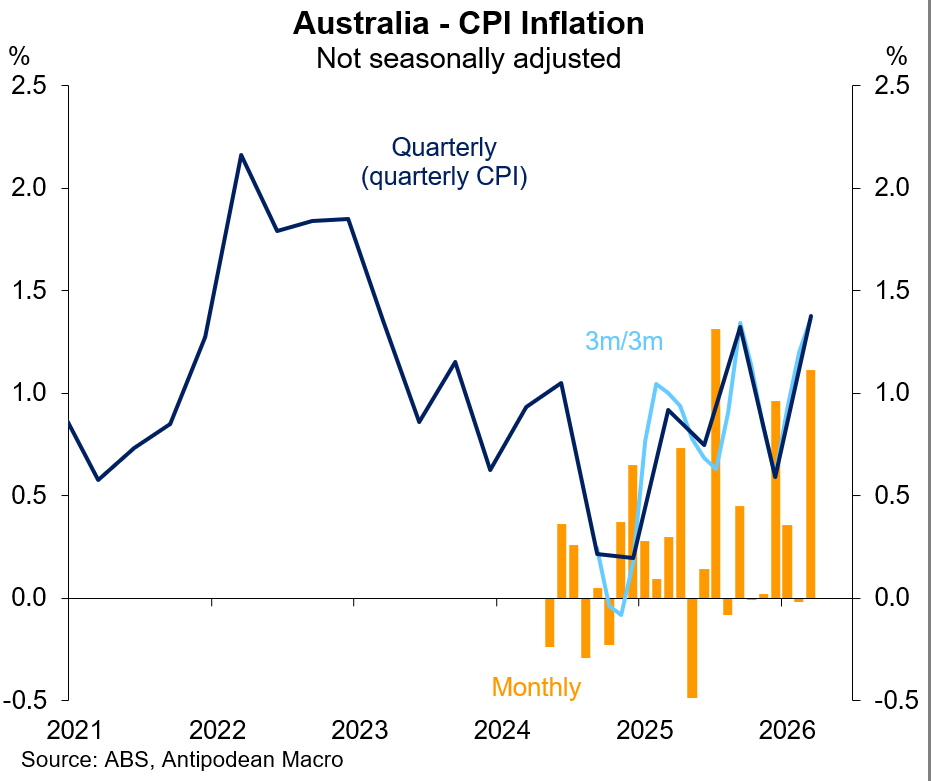

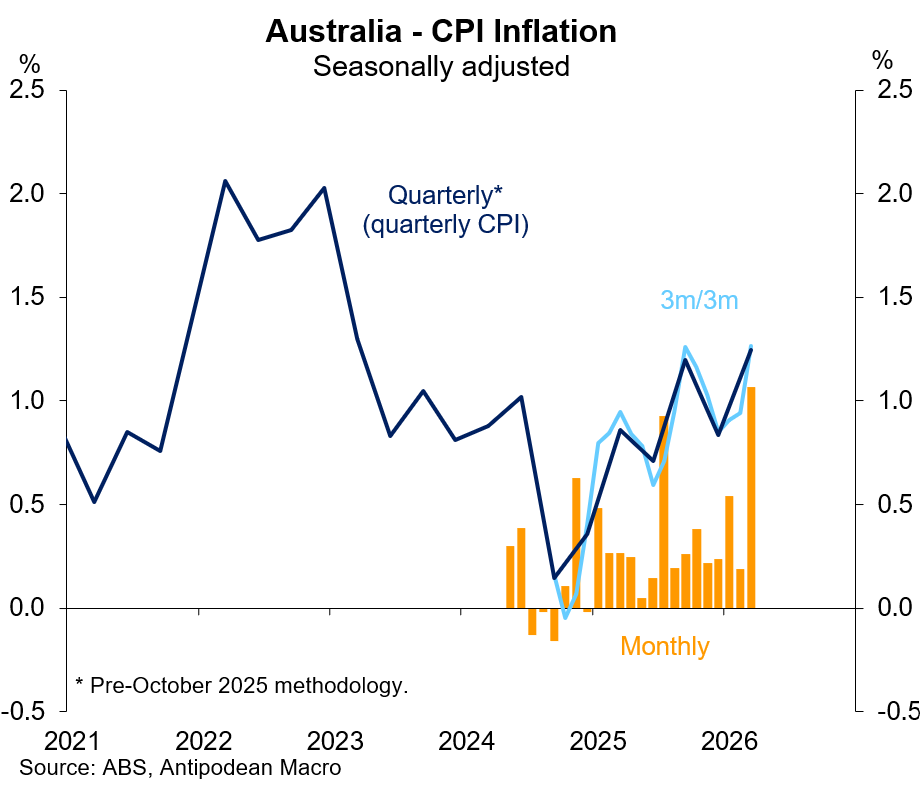

1. Australia’s monthly CPI in March rose +1.1% m/m in both original and seasonally adjusted terms. This was in line with our nowcast in seasonally adjusted terms and slightly softer in original terms.

Headline inflation was +1.4% q/q in Q1 and +1.3% q/q post seasonal adjustment.

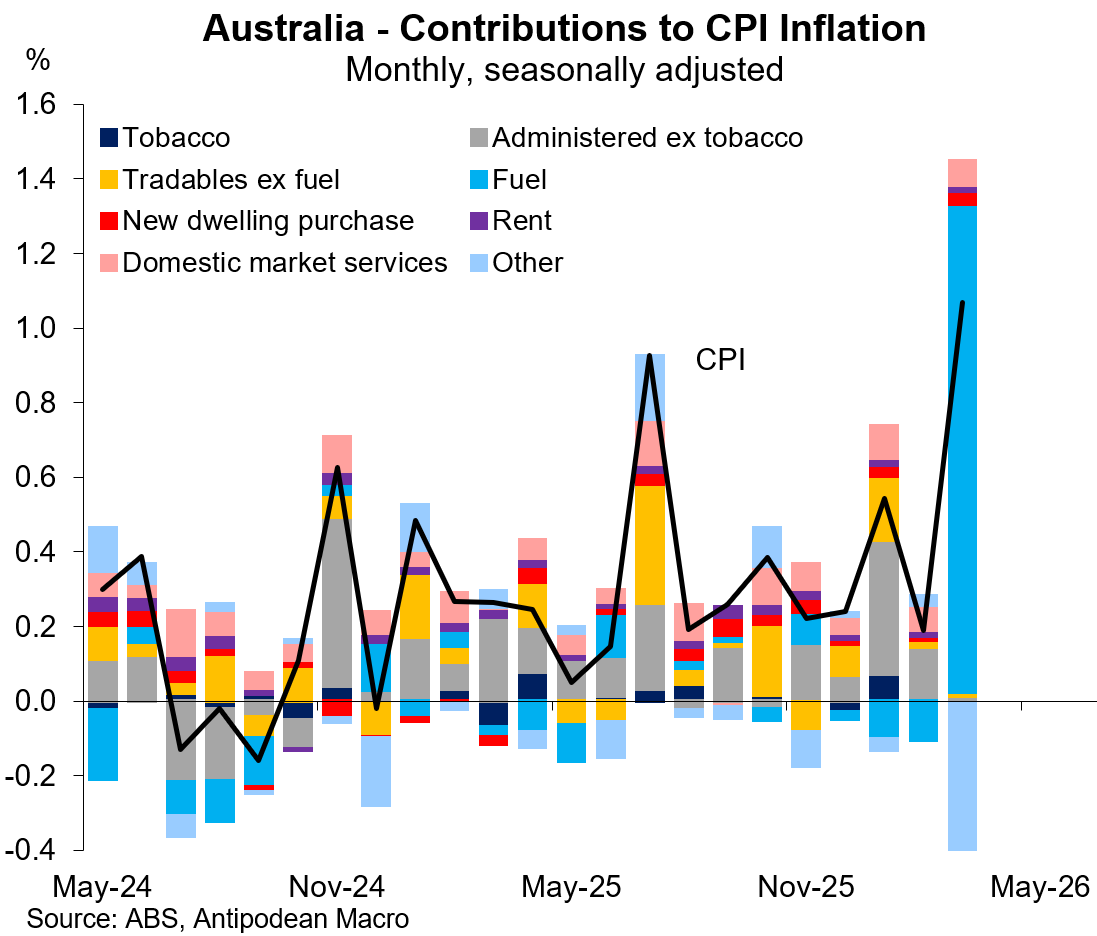

As expected, automotive fuel (+33% m/m) contributed 1ppt to monthly headline inflation in March. The main downside surprise relative to our nowcast was the volatile holiday travel & accommodation category (-1.4% m/m).

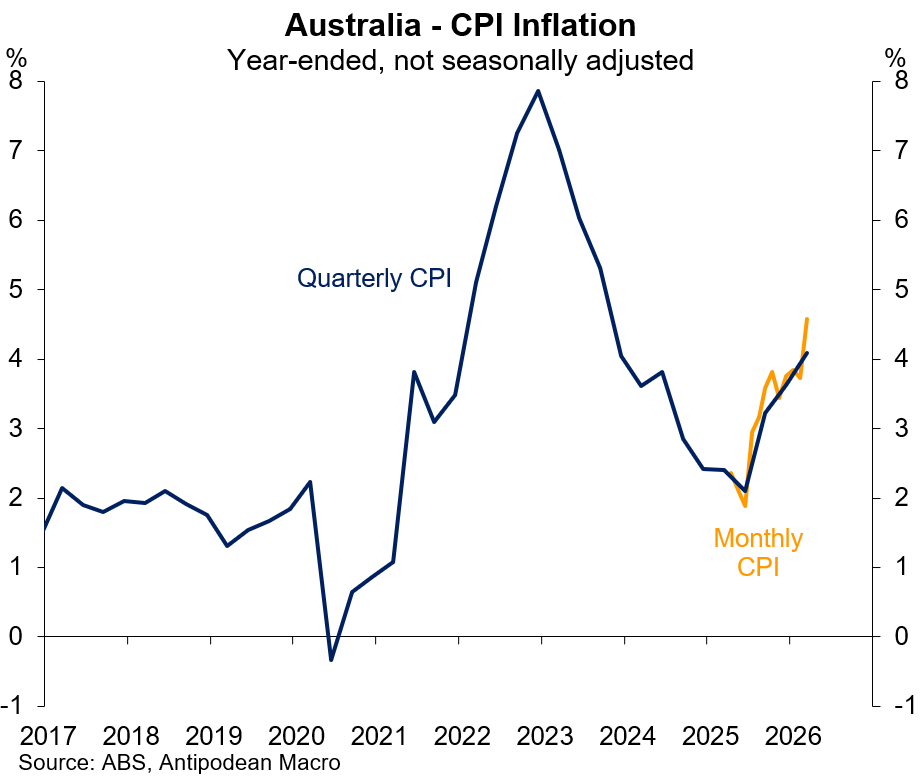

Year-ended CPI inflation was +4.6% y/y, up from +3.7% y/y in February. (Our nowcast was +4.7% y/y.)

The table below provides more detail on the CPI by key groupings, including on a 3m/3m basis.

Keep reading with a 7-day free trial

Subscribe to Antipodean Macro to keep reading this post and get 7 days of free access to the full post archives.