ONLY CHARTS is available to paid subscribers.

A 7-day free trial is available below. Group discounts are available here.

Antipodean Macro’s in-depth research is available here.

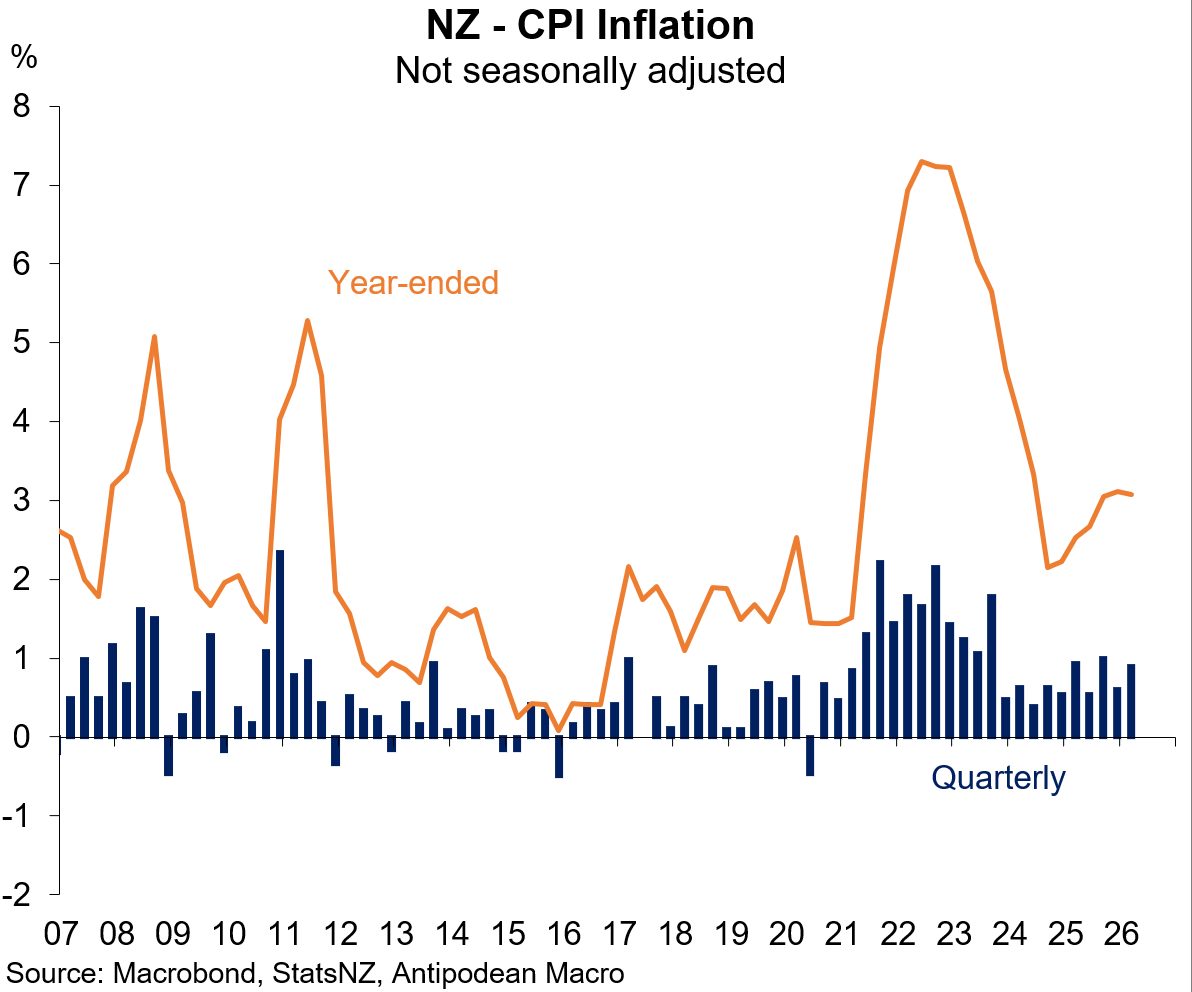

1. New Zealand’s Q1 CPI inflation was +0.9% q/q and +3.1% y/y.

This was higher than our nowcast of +0.8% q/q and +2.9% y/y. The RBNZ’s updated nowcast was +3.0% y/y.

Non-tradables inflation was in line with our estimate and only slightly higher than the long-run average in quarterly seasonally adjusted terms.

Stronger-than-expected price rises for some tradable items and pharmaceutical products drove most of the ‘miss’ relative to our nowcast.

Prices for pharmaceutical products rose +17.7% q/q - driven by an increase in prescription charges - and contributed +0.12ppts to quarterly headline inflation.

StatsNZ noted that “the prescription count for the prescription subsidy scheme reset on 1 February 2026, meaning households who had previously exceeded the 20-prescription threshold, and were receiving free prescriptions, now had to pay the prescription co-payment.” While we knew this was coming, the size of the increase caught us off guard.

In addition to pharmaceutical products, the largest contributions to quarterly headline inflation in seasonally adjusted terms were: petrol & other vehicle fuels (+0.1ppts); food (+0.16ppts; known); household energy (+0.1ppts; known) and jewellery & watches (+0.05ppts; higher gold prices).

Our measure of quarterly trimmed mean inflation rose a little in Q1 and suggested that underlying inflation remained contained, though remained above the 2% target mid-point (see below).

Keep reading with a 7-day free trial

Subscribe to Antipodean Macro to keep reading this post and get 7 days of free access to the full post archives.