ONLY CHARTS is now only available to paid subscribers.

A 7-day free trial is available below. Group discounts are available here.

Antipodean Macro’s in-depth research is available here.

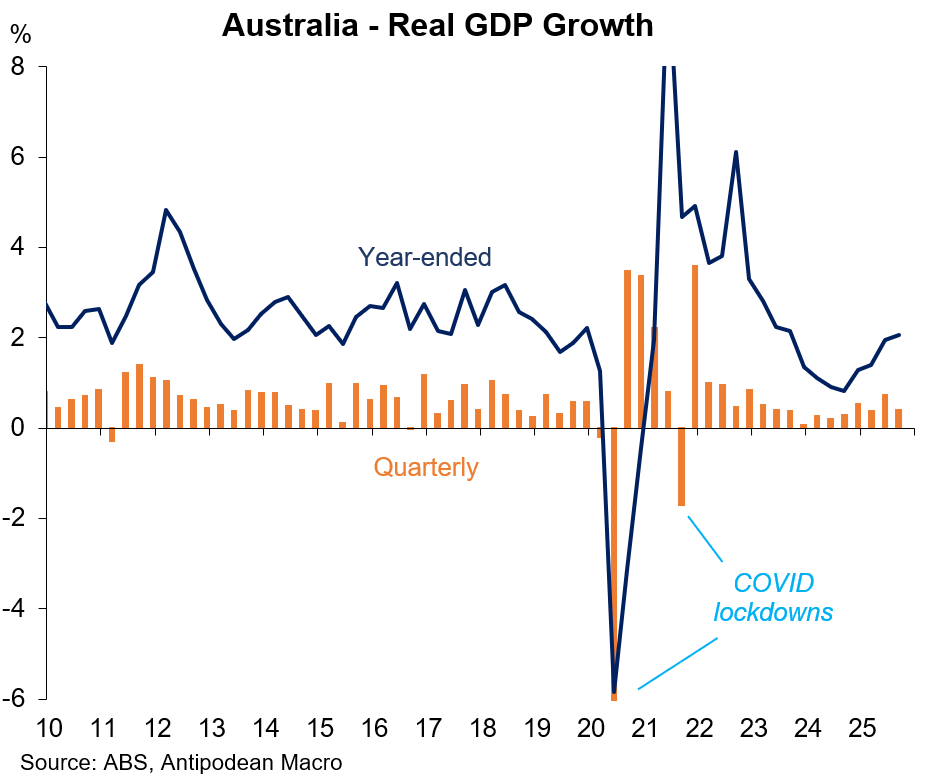

1. Australia’s GDP rose +0.4% q/q and +2.1% y/y in Q3.

The RBA had pencilled in around +0.55% q/q and +2.0% y/y in the November SMP.

Our sense is the Bank will view today’s release reasonably positively. Quarterly GDP growth has been volatile because of several temporary factors. Notably, growth in domestic final demand - particularly private demand - has picked up (see below). Ongoing strong growth in unit labour costs, however, provides a note of caution.

Quarterly growth was weaker than the +0.7% q/q we and consensus had pencilled in (though year-ended growth was only 0.1ppts softer than expected).

All of the downside surprise to our forecast was accounted for by growth in both business and dwelling investment being noticeably weaker than partial indicators suggested.

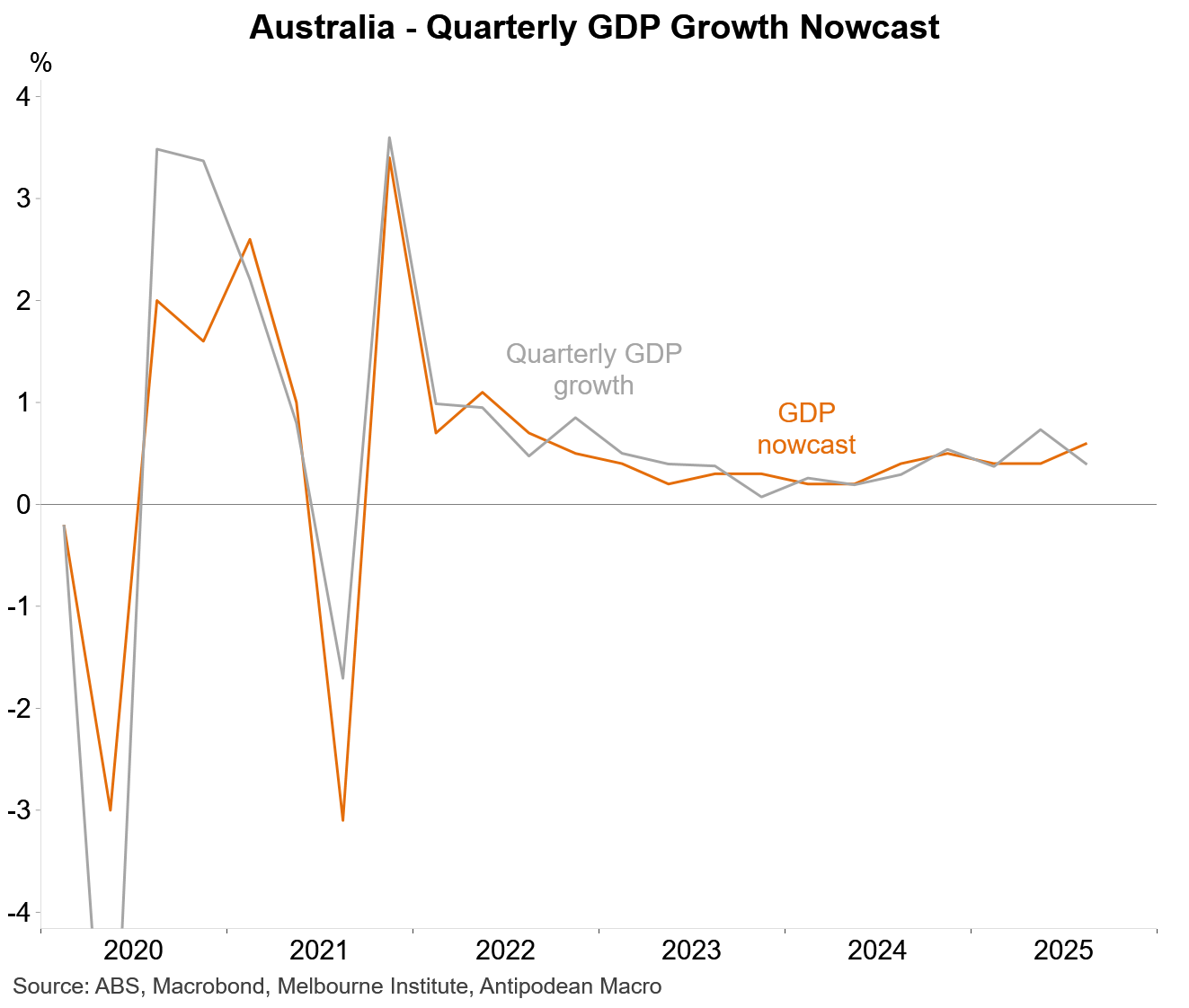

Independent GDP nowcasts also pointed to a modest improvement in underlying GDP growth in Q3 after missing the actual outcome to the downside in Q2.

Keep reading with a 7-day free trial

Subscribe to Antipodean Macro to keep reading this post and get 7 days of free access to the full post archives.